If we want to fix the entire banking system,

then we have to deal with the entire system !!!

_______________________

QUESTIONS & ANSWERS

1) Why should we put together this “One Bank”?

There are thousands of different banks and S&Ls throughout the U.S. — and they are all basically tied into being just “one system” already! The consumer foots the bill for all of these banks with their multiple branches and expensive computer systems — WE PAY FOR THEM — so what would be “less expensive”? 7,000 banks or 3,000 banks? . . . 3,000 banks or 1,000 banks? . . . or 500 banks . . .? Obviously, we will end up considering having only ONE bank!

2) Why would this “One Bank” not need to foreclose on people?

I worked in a bank for 5 years — and there is ONLY ONE REASON why banks “foreclose” on people — they foreclose if you cannot pay your monthly payments! The one and only thing that banks and savings and loans are concerned with is GETTING THEIR MONEY BACK — and if you fail in paying back their money, they will FORECLOSE on you! So here’s the Big Question:

Would a bank that ALREADY HAS ALL THE MONEY ever

need to foreclose on you to “get their money back”?

**NO!!!**

IT ALREADY HAS

ALL THE MONEY !!!

This is the all-important concept to keep in mind, this is the

linchpin that solves the entire system — would a bank

that already HAS all the money ever need to foreclose on

people to get its money back?

Why would it?

IT ALREADY **HAS** ALL THE MONEY !!!!

Why would it work that way?

BECAUSE THAT IS HOW WE

SAY IT WILL WORK !!!

* * *

3) What happens in the present banking system when a bank makes a mortgage loan?

After a mortgage loan is made, our current banks just sit there “waiting” for their money to come back, and this can take as long as 20-30 years — and every one of our banking institutions desperately “needs that money back.” When they make an $80,000 loan to someone to buy a house, the buyer takes that money and pays it to the seller, and the seller PUTS IT INTO THEIR BANK, and that bank now pretends that THEY “have that money” — and this bank only has to keep “10% of that money” on hand, and they can loan out $72,000 to ANOTHER customer — and on and on the money goes from bank to bank to bank, over and over and over again… and again… and again…

4) Geometric progressions of money!

U.S. NEWS and WORLD REPORT did an extensive 28-page article about the “ABCs of Today’s Economy” in their April 26, 1982 issue — and on pages 48-49 they showed how money is geometrically increased within our banking system. If the Federal Reserve System wants to expand the money supply by $100 million they purchase $10 million in U.S. Treasury bills from a securities dealer — the dealer deposits the Fed’s check into Bank A and $10 million is added to the money supply. Bank A keeps 10% and loans out 90%, thus adding another $9 million to the money supply. Bank B does the same thing, loaning out $8.1 million — Bank C will also loan out the 90% of the deposit, etc., etc.! It happens again and again, and again, thus $100 million is put into circulation! (If you want to see this chart that was in this issue, I can e-mail as 3 attachments upon request.)

5) Didn’t they just create money out of thin air?

YES, THAT IS EXACTLY WHAT THEY DID!

We can easily say that 90% of all the money in circulation is money that has been created right out of THIN AIR by our banks!!!

Under today’s system, this can be extremely dangerous — but I am going to show you how it can be done in a “painless” and beneficial way.

6) There are 2 forms of INFLATION — are both “bad”?

The 1st form of INFLATION is when the amount of money in circulation is increased — and this usually leads to the 2nd form of INFLATION, the raising of the prices on goods and services. This has been why the Fed has to be very careful about putting more money into circulation — because people will raise their prices, and our money can become “worthless”!

7) Is there a way to “inflate” the amount of money in circulation without people “inflating” their prices?

YES, there is — by letting people know that the “One Bank” would NEVER FORECLOSE on them no matter what their monthly income is!! Would people need to raise their prices if “it didn’t matter” how much they paid back to the One Bank each month for their mortgage payment? The pressure would be off — people could relax! There would be NO NEED to constantly “raise” one’s prices on goods and services! (I would assume to actually see prices LOWERED if and when the One Bank would be up and running! A “dollar” could once again become something that is really worth a “dollar”!)

********

The Number “Zero”

Have you ever thought about numbers, the number “zero” in particular? The earliest known written sample of the number zero dates back to 870 AD (it was created by a mathematician in India), and during those early days the “zero” was thought to be a strange and mysterious thing — some people even thought it was “of the devil”!

30000000 00000003

If you take a number and put a zero behind it, you increase the value of that number ten-fold — but if you put that same zero in FRONT of that number, it does nothing! And this upset a lot of people back then.

We are descended from people who could barely bring themselves to understand and accept the use of the “zero”! Face it,mankind was pretty IGNORANT back then — but is it any different now?? People always price things at “$19.99″or “$49.99″and hope we won’t notice that the REAL cost is $20 and $50! DUH! Merchants count on “fooling” us with their prices on things because they know that the human mind has problems dealing with NUMBERS, and that has been the very problem that “inflation” has caused — economists hate dealing with that pesky “zero” being added and added onto numbers and “inflating” the amount of money in circulation! But with only One Bank around, WE CAN CONTROL THOSE ZEROS AND USE THEM IN A WAY THAT THEY WILL NOT DO ANY DAMAGE on the computer systems of the benign One Bank system!!!

The FIXX’s 1983 song “Saved by Zero”

Who knows? Maybe our banking system can be “saved by Zero”!

Hey, this might be a great theme song for this webpage and entire banking solution!

Here’s the YouTube link to listen to the song:

https://www.youtube.com/watch?v=JOiZP8FS5Ww

8) What would come of the mortgage money that is repaid back to the “One Bank”?

THAT MONEY WOULD BE

*DE-INFLATED* RIGHT BACK

OUT OF EXISTENCE, right back

to where it originally came from!

It was created “out of thin air” so that it could geometrically increase to provide someone with a house loan, right? We let money “inflate” when needed, and then let it “DE-INFLATE” out of existence when it’s paid back to the One Bank! Would it matter to the One Bank? No — because no matter how “big” or “small” the numbers are on its computers, IT WON’T MATTER! This One Bank will ALWAYS have “all the money,” no matter what those numbers are! And for the first time in human history people will no longer be afraid of “inflation,” either form of it.

9) So what would your monthly mortgage payment be?

It would depend upon what you earned — I assume it would be a fixed percentage of a person’s income, say perhaps 25%. If you made a lot, you’d pay a lot — if you only made a little, you would only pay a little. Why would this be a problem with the One Bank? Does it really need your money back? Remember, IT ALREADY *HAS* ALL THE MONEY!

10) Would the “One Bank” help ease the pressures of the rat race?

There is no doubt about it — if people wanted to reduce their work hours, they could do it! If people wanted or needed to take time off to attend school, they could do it! Why would the One Bank not let people do this? Is the One Bank worried about not getting its money back from you? IT ALREADY *HAS* ALL THE MONEY!! People could SLOW DOWN — and live their lives at a much better pace.

11) Would everybody be able to stop working?

What about “DIRTY JOBS”?

People have a tendency to be really “lazy,” but this system is NOT going to be set up just so everybody can “avoid” doing their jobs and facing their responsibilities. I would assume that the work week would be somewhere between 20-30 hours a week, and I would think that in most cases that would be mandatory. There is NO WAY we would let society permanently stop working and “grind to a halt” — Mike Rowe’s DIRTY JOBS will still have to be done, and we can all discuss a way for this unfortunate fact of life to be arranged.

12) Who gets a mortgage loan?

EVERYONE can get a loan for a home — EVERYONE! Why won’t our current banks make a loan to a “poor person”? Because they won’t get their money back! But when a home loan is made to a poor person in the One Bank system, that money IMMEDIATELY returns to the One Bank when the builder or seller is paid — no longer do we have a banking system that is afraid that they will not get their money back, so home loans can be made to ANYONE no matter their income!

We could immediately fund

and begin building MILLIONS of

new homes as soon as the

One Bank System

is put in place!!!

THIS WOULD CREATE

50+ MILLION NEW JOBS!!!

13) Is it “fair” to give unemployed people a loan for a home?

The poor people on this planet have suffered enough — this is the 21st century and it is time to end this system of dumping on the poor! IT’S GONE ON FOR THOUSANDS OF YEARS, AND THAT’S LONG ENOUGH!!! The One Bank would have no trouble making home loans to poor people, and we could even start building houses out of compacted dirt or concrete like Thomas Edison first designed back in the early 1900s — there’s NO NEED to cut down every tree in sight just to build more homes! Is this “giving free money” to people who won’t work? NO!! The “money” will get paid to THE PEOPLE WHO BUILD THE HOUSES — not to the people who live in them! People who WORK will be people who GET PAID FOR THEIR LABORS!

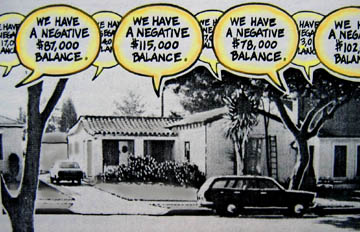

14) What about the poor person’s “balance due”?

Look at the bank balances of all of the people who already “own” their own homes! ALL OF THESE PEOPLE HAVE *HUGE* NEGATIVE BALANCES! If you have only been paying on your house for a few years, you have a GIANT NEGATIVE BALANCE at your bank — so why not let a poor person also have “a giant negative balance”? Remember, the One Bank already HAS all the money — why would it care how fast you or that poor person pays off his mortgage loan?

15) Who really “owns” your home?

BANKS really own all the homes around this country, unless you are fortunate enough to have actually paid off your house — now, would you prefer to have your home “owned” by a single bank that would never need to foreclose on you, or would you prefer to have your home owned by a bank that CAN foreclose on you?

Here’s what our neighborhoods look like now, every single home owner has a huge negative debt:

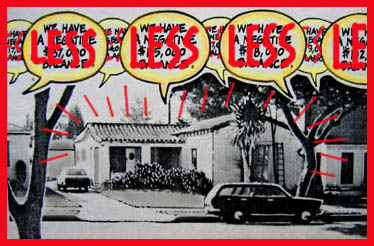

… and here’s what that neighborhood will look like after the One Bank is established:

… all mortgage debts would be REDUCED since most of that debt is collected interest to finance the thousands of individual banks….

ALL THE HOMES WILL STILL HAVE SOME SORT OF NEGATIVE DEBT, BUT THE ONE BANK WILL NOT BE CONCERNED ABOUT HOW LONG IT TAKES TO REPAY THOSE DEBTS!!

ADDED NOTATION: Obviously implementing this idea to the whole country all at once would be far too risky, so what we would need to do is first try it in a couple states. I would suggest we pick states that have a lot of wide open space available for building new homes, and where the farmers grow some major crops so we can assist them — set up a “One Bank” system in those areas and study how it affects the local community and how the impact ripples out to the areas that are not under the One Bank system! If it WORKS, then we expand it into other states! The idea would be to make the change over to the new system “slow and easy” — and if we find out it doesn’t work, then we just stop using it!

* * *

16) Has mankind’s “money” system been evolving?

“Money” started out by being gold or jewels or coins with emperor’s egos stamped on them — then “paper money” was made, and people thought it was valuable because it was backed by gold or silver, but all that ended in 1971 when the U.S. went off the gold standard! Now money is NUMBERS ON COMPUTERS — completely intangible numbers on all of these COMPUTERS!

Here’s what your money really looks like:

It’s just numbers on computer chips!!!

Yes, “money” has been evolving over the years — and if we let it evolve just ONE MORE STEP it will have reached its final goal! “Money” can finally get off the back of mankind, and merely be a tool for measuring people’s individual productivity within society. I find it rather amusing — the “solution” for our banking system has been printed right there on our money all along…

“E pluribus unum”:

OUT OF MANY, ONE !

17) How do we deal with the “duality” of the money in our banks?

Banks have always loaned out that 90% of their deposits, and by doing so they have created 90% of the money in circulation out of thin air — and when they did this, they established large negative balances on their computer registers. So how does “money” exist within our banks? It is there as POSITIVE BALANCES (the money in our checking and savings accounts that we can SPEND), and it is there as GIANT NEGATIVE BALANCES that are on the books for years and years and years! So which balance is the “right” balance? The positive or the negative balance? THEY BOTH EXIST! Therefore we need to get used to the idea that “giant negative balances” in the One Bank is a natural and NORMAL thing! It’s just that everybody would now get a chance to have their own “giant negative balance” in the One Bank system, because this is a bank that provide a mortage loan to every single human being in America! And it’s a bank that will never foreclose because it always *HAS* all the money!

18) What if today’s bankers don’t want us to set up the “One Bank”?

Most people think that big banks are all-powerful institutions, and there’s no way that “we the people” could ever tell them what to do. Well, here’s how “powerful” all those banks are: If you want your money out of those banks and put into a better bank, ALL YOU HAVE TO DO IS GO INTO THEIR BANKS AND “ASK” FOR YOUR MONEY TO BE TAKEN OUT OF THAT BANK! That’s not a very”powerful” bank, in my opinion! Now, I in no way want to endorse doing “runs” on existing banks, but I want all the bankers on this planet to understand that if the people of the U.S. want a “One Bank” that would never foreclose on them, then today’s banks are going to have to LET US HAVE that One Bank!

19) How would we switch over to this “One Bank”?

First we would test the system in a few areas of the country, then, if it works, we would convert the thousands of existing banks and S&Ls into the “One Bank” system and close down the branches that are not needed. Guess who really “owns” all those thousands of existing banks? WE DO! THE AMERICAN PUBLIC! All those buildings and all those computer systems WERE BOUGHT WITH **OUR** DEPOSITS, OUR MONEY, THE MONEY WE GAVE THOSE BANKS! OUR MONEY, NOT THEIRS! Yes, it would be a “big job,” but if you want the system fixed, YOU HAVE TO FIX THE WHOLE THING — and that will entail merging everything into a single system, just a bit more so than it already is — is this “too big a job”? It’s going to take some work to fix the “entire” banking system — so we either DO IT, or we don’t. All the accounts that currently exist in all of our nation’s banks would continue to exist right as they currently are, but linked to a One Bank system. The interest rates on all of these loans would be readjusted down to a more reasonable level — the One Bank will NOT be a “for profit” business, it will ONLY charge what it needs to pay its workers to make sure the system keeps running.

20) Can a man in a financially depressed area get a loan from the “One Bank”?

Of course he could! With electronic banking we no longer need to worry about just making “regional” loans — no longer will out-of-the-way areas be financially depressed areas! And this “One Bank” will NEVER say that it “cannot find” the money to make you a loan — but we will have to decide exactly what these loans will be given for, and I assume it will mainly be housing. If people want to buy a car or a stereo, then they GO TO WORK TO EARN IT. We can heal our poorer neighborhoods! We could fix up all the houses that are on “the other side of the tracks”! POVERTY WILL COME TO AN END! After floods or hurricanes hit and destroy people’s homes, the One Bank would have NO PROBLEMS issuing new mortgage loans to those people like for the folks who got hit by Hurricane Katrina, etc.!

21) Would the “One Bank” be a monopoly?

NO ONE WILL OWN THE “ONE BANK” — no private individuals will have private access to this bank’s money! Again, we already technically have a “one bank” system — all of our existing banks are interlinked into what is really just “one system” — (it’s been widely known that if one or two of our “big banks” crashed, the ripple effect would also bring down hundreds of other smaller banks, if not our entire economic system around the world!) — so I am absolutely sure that there is a way to put together this “One Bank” so that it can be a totally BENIGN “monopoly” and nothing to fear, and it would be a bank that would NEVER “crash”!

22) What about Bankruptcy?

With the One Bank system NOBODY would need to file for bankruptcy! Why? Because a person’s income is positive & negative numbers on the One Bank’s computer system, and that bank that is not concerned with how fast their mortgage loan is repaid — a person’s income is a person’s income, and the One Bank doesn’t care what the numbers are!

23) It’s “Money vs. People”!

Which is more important? Money or people? For centuries people have been evicted from their homes and their land just because some banker “held the note on their property” and those families had financial problems, and people were locked up in “Debtors Prisons” — AND IT’S TIME FOR THIS TO STOP!! People need to understand that it IS possible to have a completely BENIGN banking system in this country, one that is not constantly perched over our heads like some kind of demonic vulture waiting to spring upon us as soon as our funds “come up short”! I’M REALLY TIRED OF IT, and I know that millions of other people in this country are ALSO good and tired of it. Families can’t spend quality time with their children because they are too busy running the rat race — and the poor are set up to STAY POOR, except for the rare few who manage to overcome their dead-end living conditions — THIS IS A CRIME — AND IT DOES *NOT* HAVE TO STAY THIS WAY!

24) Paying Our Taxes

Paying our taxes could be simplified by it being just a “flat tax” for everyone, just a certain percentage of each person’s income — and maybe it could even be paid on a monthly basis — but it would be a totally PAINLESS process, because everyone would be dealing with a bank that never forecloses no matter what their income is! And these taxes would go to the things that taxes already go to (and not to some things they currently go to, because that would now be unnecessary!…) Here’s a new category that we might consider adding…

25) Payment for Housewives!?!?!

YES! We could set up a fund that would be for paying housewives for working at home! After all, it *IS* work! Whoa, now that’s a great idea… (and maybe “home husbands” too)….

26) Health Care & Medical Costs…

How can we deal with the astronomically high doctor/hospital bills and drug costs, etc.? First, we need to understand that sometimes it costs what it costs to do the right thing and HEAL people, and we shouldn’t worry about how many negative numbers are pulled out of thin air on the One Bank’s System to take care of the sick and elderly!! And the same applies to those students who have to finance 8+ years of medical school to learn to become a doctor or a surgeon — what’s so bad about letting “negative numbers” remain on the One Bank’s System? Negative numbers are going to be there FOREVER on the One Bank System no matter what people do or how fast they pay back their loans.

Here’s how the new Health Care System would work: The One Bank that “has all the money” pays everyone’s medical bills — and then 2 sources of repayments are set up: 1) The people who received the hospital’s services pay as they can afford it, and 2) Society begins paying towards ALL of the hospital’s balances due (via being taxed), but we must remember that all these medical bills are just another “negative number” on the One Bank’s records, and this One Bank is set up to deal with long-term negative numbers without any problems — so IT WILL NOT MATTER how long it takes to pay off a medical bill! But NO ONE loses their home in this process!! NO ONE!

No Death Panels!

No cutting off critical care!

_____________________________________

27) The HUGE National Debt

See the National Debt Clock at www.usdebtclock.org

$25,711,800,000,000+++

Our National Debt will cripple our future generations and can make every person in America an indentured “slave” to the “masters” we are in debt to — but the One Bank system can solve this problem too! It’s this easy: Instead of taking in the mortgage payments from everybody in the country and “vanishing” it out of existence, we put that month’s mortgage payments all towards the National Debt! It would be done periodically as many times as is needed to pay off the entire National Debt — which makes the paying off of the National Debt to be totally painless! It’s all possible because we would have a bank that “has all the money” and was not needing all those mortgage payments back to stay solvent (it ALWAYS “has all the money”) — and those mortgage payments were just inflated money that was just going to vanish out of existence anyway — so why not keep it in existence to pay off the National Debt? As long as that money is linked to a stable American economy, then it’s good money whether it stays here in the U.S. or it goes to China or anywhere else!

28) Do we want to build a wall on the US/Mexico border?

THEN BUILD IT! Oh, you can’t find the money? Excuse me, in a One Bank system there’s no problem “finding the money”! But then again, why not just grant those people citizenship and give them a loan to build themselves a home that would never foreclose on them….?

* * *

What about “Reparations”?

With this One Bank system we could seriously consider paying reparations to all the people who have been mistreated by our country!

“ONES”

If needed, we could keep track of this One Bank money by calling it “Ones” (an example is if I receive a payment for work of $850 from the One Bank, it could be notated as “$850 Ones” within the system or in regular banks that receive the money). The One Bank dollars will still be worth the same value as pre-existing dollars (which, I remind you, have been created by pulling 90% of them out of thin air!) — so there is no reason to be worried about the One Bank money, it’s really just as real as the money that’s already in your bank!

“Money” exists for us to get things done — SO LET’S SET UP A FINANCIAL SYSTEM THAT LETS US GET THINGS DONE!

____________________________________________________

The Space Program

What about financing NASA’s space program?

Frankly, as far as I care, we should inflate as much money as is needed for certain things like the space program — and I don’t really care how it affects “inflation” or “the price of gold” — CERTAIN THINGS IN THIS WORLD NEED TO BE DONE!!

* * *

Every Country is in Financial Trouble!

Can this One Bank solution can be expanded to include the nations in Europe, and maybe even the entire world?

If it can work for one country, the United States, it should be able to be expanded to work for the other debt-ridden nations of the world — if these nations can learn to “cooperate” and concentrate on working it out!

…Yeah, like there’s a chance of that ever happening….

________________________________________

DIAMONDS

This is the type of “diamond” that most people have on their minds….

…but now take a look at this DIAMOND:

This is an electron microscope photo

of a DIAMOND NEEDLE

PLAYING A PHONOGRAPH RECORD !!!

A diamond needle!!!

It is ABSOLUTELY AMAZING that dragging a diamond needle down those groves can produce “music”!

Diamonds were not made just so people can wear them in rings and necklaces to inflate their egos and show off how “rich” they are — diamonds are SPECIAL in other ways — but it’s up to each of us to see it.

Whenever people tell me that something “can’t be done,” I like to remind them that we live in a world where several extremely AMAZING THINGS can be accomplished!

Is it “impossible” to put together a Bank that won’t foreclose on people??

Miracles CAN happen, and this can

apply even to FINANCIAL MIRACLES!!

I say we can fix our banking system!

_______________________________________

GOLD

Everybody is talking about investing in gold, as if it’s the “oh-so wonderful solution” to everything.

But it isn’t.

Not everyone can invest in gold — but everyone DOES use “money”! So a solution to our economic system must mainly focus on our banks and the computerized numbers within them that are society’s real money.

Should we ever go back on to the Gold Standard?

!!!***NO***!!!

Having our money backed by gold would be the worst thing in the world to do — “money” needs to increase and decrease depending on the needs of society and how many homes need to be built, “money” should NEVER be dependent upon how big a pile of gold we have on reserve!

Gold wants to be

Mankind’s #1 Pet Rock!

Far too many people are addicted to this “Pet Rock”

Sure, it’s valuable — sure, it’s value keeps increasing while the value of “money” drastically decreased in the past few years — but gold is NOT the solution to our financial problems!

________________________________________________________

I lived in the Washington D.C. area in 1985-1988

I printed up this flyer and tried to get people to pay attention to my banking solution:

I met with Mr. Pat Berbaccus at the old Federal Home Loan Bank Board, and after I explained my ideas he agreed with me that I was right! I asked if I could get a local reporter to interview him would he tell that “on the record,” and he said he would — but the local newspaper reporters were so used to saying “No” to me that none of them would listen to me about interviewing Mr. Berbaccus!

So nothing happened there in D.C. back in 1985-1988

I’m not surprised, it’s nearly impossible to lobby to get anything done in D.C. unless you have a big organization behind you and lots of $$$$….

More Q & A

The New York Stock Exchange and Wall Street have not been “behaving” themselves the past several years — I think it’s pretty obvious that we need to do something to permanently correct this faulty system…

1) The “NEW” New York Stock Exchange — If people want to invest their money in the Stock Exchange, they can. If that company makes a profit, they get the money due them. If the stock does not make money, they lose their money — but they still have a bank that will NEVER FORECLOSE on them, so the pressure of having to always make a profit vanishes! Hey, we might actually be able to invest in really BENEFICIAL THINGS like solar power, etc., the things that are now seen as being “too costly” to pursue!

2) Bank Stocks — People own stock in various banks, and banks are set up to earn a profit for their are holders, but this will not be necessary if there is only One Bank. The money that people have invested as shares will immediately be added to their bank account.

3) Banks as “For Profit” Institutions — The One Bank will not be a “for profit” bank. It HAS all the money, and people will either earn their income and have it credited as positive numbers in their accounts, or they can invest their money in companies via “New and Improved” Stock Exchange.

4) Interest — The One Bank will no longer have to compete for deposits, so it will no longer have to pay out interest on savings deposits and CDs, etc., which lessens the bank’s need to “make a profit” on its investments. Again, the pressure is eased off the system, which is the main benefit here in this entire One Bank system!

5) Schools — Another benefit not previously listed is that people could now take “time off” from work to be able to attend school — “illiteracy” has always been a major problem for societies to deal with, and the fact of the matter is that “poor people” cannot afford to get themselves an education. I don’t know about you, but I am sick and tired of this vicious circle of people being “poor and uneducated” just going on and on — PEOPLE NEED TO BE ABLE TO GET AN EDUCATION!!! And if this One Bank system was set up, those people would finally be able to GET an education! How? Because they could take the time go to school and NOT HAVE TO WORRY ABOUT GETTING KICKED OUT OF THEIR HOMES!

6) “Renters” — While I’m at it, I might as well also tell you what would happen to people who “rent” homes or apartments — our current system has been very unfair to the renter — renters end up paying for a house that SOMEBODY ELSE GETS TO OWN, and this needs to stop. In the new system all renters will be accredited his or her portion of their financial investment of that house or apartment building on the One Bank’s computer system — apartments and some houses will now have “multiple owners,” depending on who has paid how much into the house or apartment. Is this a fair thing to do? Remember, nearly all the homes and buildings in the world are ALREADY “owned by the bank”! Do home owners really “own”their houses? NOT IF THEY HAVEN’T FULLY PAID OFF THE BANK! YOUR BANK REALLY “OWNS YOUR HOUSE”! In the One Bank system this situation would still be true, the One Bank would own EVERYTHING — but so what? The “home owners”who lay claim to those buildings will have the control and say-so of what happens to their buildings, just like they do now — but all those home owners and “renters” will be facing a bank that will NEVER FORECLOSE on any of them!

The whole idea here is to finally

make the system “fair” to everyone!

WE NEED TO BEGIN A

NATION-WIDE DISCUSSION

ABOUT THIS

BANKING SOLUTION !!

* * *

What about dealing with Natural Disasters?

Tornados & hurricanes & floods are increasing and destroying homes and property — the One Bank would have no problem issuing new loans to all of these people to re-build new homes!

And what about their old mortgage debts?

Hey, if “An Act of God” can wipe out people’s homes,

then “An Act of the One Bank” can wipe out those previous debts!

Each family’s mortgage debt on their destroyed home would be erased, and then they would be assigned the new debt of building the new house — and face a “One Bank” that would not be concerned at how quickly they repay the new mortgage loan.

IT’S TIME TO DESIGN THE TYPE OF

BANKING SYSTEM THAT WE WANT,

NOT ONE THAT DESTROYS & CRIPPLES US!!!

This would also alter the need for people buying House Insurance or Flood Insurance — why would they need to buy insurance if the One Bank just issues all those people a new loan for a new home to be built? No one would need to buy insurance for their homes!

Oops, I just simplified the whole system again…

* * *

Here’s a good phrase to keep in mind:

“If money still talks,

it should be apologizing…”

The money system of the world has been “evolving” throughout the centuries — and the entire economic system of this country, and maybe the entire world, can be PERFECTED if we will allow “money” to take this one last evolutionary step and let all these “numbers on computer chips” function benignly on the One Bank’s system. This inequality of the rich ruling economically over the poor has to stop, and stop soon, or we will one day see an escalation of hostilities enacted by the “have nots” in our society!

I really don’t look forward to all the “arguments” that this idea can generate from world’s economists, but I still hope that we can hold a nationwide discussion about the merits of this One Bank idea.

**********

I hate to be crude, but sometimes a person has to be somewhat blunt…

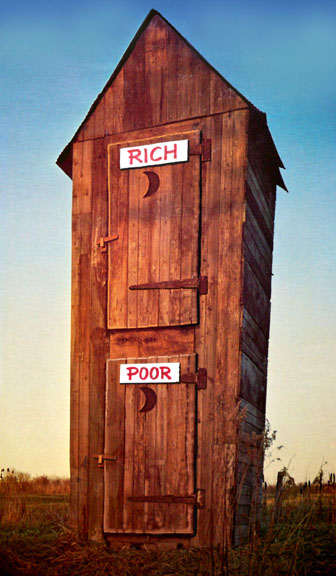

“Capitalism/Crapitalism”

Many years ago I found this poster of a 2-STORY OUTHOUSE, and it illustrates the situation very aptly — the RICH are on top, and the POOR are on the bottom….

If societies set up economic systems that allow the affluent few to constantly “dump” on the people who are poor and less affluent, then you are raising up societies that will have lots of poorer people who will become extremely upset with rich people…. and we all know what can happen next when the disenfranchised finally get totally fed up! Riots… destruction …and people walking around wearing T-shirts saying, “Eat the Rich”…

It’s time to solve this mess and put a system in place that lets EVERYONE participate in the joys of modern society.

* * *

The Way GOD Set Up His Banking System

The Sabbatical Year/Jubilee Year

Every 7 years ALL DEBTS were supposed to be annulled!

This is how GOD told the ancient Jewish people to deal with all their financial matters — GOD knew that periodically “wiping the slate clean” was necessary — imagine if the whole world followed this counsel! I can just see all the bankers around the world saying, “Are you crazy?? We can’t cancel our loans and erase your debts just because you lost your job, we have to hold you to that debt FOREVER and foreclose on you!!”

And here is the end result of that behavior:

Our current economic system all around the world is going to IMPLODE & FAIL & COLLAPSE from all this bad Karma!!!

My banking solution is GOD’s “last ditch effort” to correct the banking system and “make things right” for everyone on the planet — IF people will go along with it!

* * *

Projected Budget Shortfalls

Nearly every state in this country is going to be facing budget shortfalls!

Every state needs to “find the money” to be able to finance the things we need to do to keep society operating — the current economic system is NOT letting us do it — so let’s put a system in place that will actually let us do what needs to be done!

It’s time to fix the system!

* * *

Need Fresh Water?

There’s been a huge water shortage in Southern California for years — yet the Pacific Ocean is only miles away…

Gee, too bad we can’t find the money to build huge Desalination Plants…

The One Bank system would have no problem funding them!

* * *

Over 65,000 Bridges in the U.S. need to be fixed!

Gee, too bad we can’t afford to fix them….

YES WE COULD FIX THEM, WITH THE ONE BANK FINANCING THE REPAIRS!

* * *

“A Beautiful Mind” — the movie & book

UPDATE from back on 1-8-2002: This week my wife and I went to see the new movie about John Nash, and I found it very interesting. First of all, I felt the movie was very poorly named, because while this man may have what some would call a “brilliant” mind, it was an extremely sick mind — and there is no way I would want that “beautiful mind” inside MY head!

John Nash was awarded his Nobel Prize in Economics in December 1994.

Many years ago back when I was first developing my banking solution, I knew that, if it was ever instituted, it would be deserving of winning a Nobel Prize. After all, I think that would be totally reasonable and a fair assessment if some person ever came up with a far-reaching solution to our economic system! But unfortunately with the way “the world” works, creative and brilliant people often get to spend many years floating around in complete obscurity while they wait for their ideas to get noticed…

The biography of John Nash made the point that a great many scientists and philosophers have had “strange and solitary personalities” — and I can relate to one aspect of John Nash’s approach to coming up with his Nobel Prize winning theory:

He joined no school and did his creative work without guides or followers!

The same way I came up with MY banking theory!

If and when my banking project is ever widely discussed, I know that one of the criticisms I will face is that I never took a single economics class at any university — I was never “indoctrinated” into being taught how things “have to work” in the economics field — BUT THIS WAS A BLESSING BECAUSE IT ENABLED ME TO “THINK OUTSIDE THE BOX” AND TO LET MY MIND GO IN A DIRECTION THAT SCHOOLING WOULD HAVE PROBABLY PREVENTED ME FROM GOING!

When John Nash was 21 and wrote his award winning theory about “games” by coming up with an idea that was TOTALLY OUT OF THE NORM — and that is what I too have done, I was 31 when my “bright idea” about solving the economic system popped into my mind.

And here it is, 33 years since I came up with my ideas — and I’m still waiting to see if anyone will pay attention to what I’ve done.

* * *

My 1983 Banking Solution Pamphlet

Hey, I really tried to get people to notice my solution!

* * *

A Short Note about my Father

My father was an accountant who became the Finance Director of a major California city, and in 1974 he was President of the statewide organization of finance directors called CSMFO, the California Society of Municipal Finance Officers (http://www.csmfo.org/about/leadership/past-presidents/ ) — he retired in 1985 — and my Dad told me an interesting story that happened to him in one of his economics/business classes at college right after WWII:

The professor put forth a scenario and asked the class for their opinions — the entire class voted for one conclusion, and my Dad and only my Dad disagreed with them and stood his ground against “the popular opinion”– and the professor told the class that my Dad was RIGHT!

I don’t care how many economics people tell me my project is “wrong” and cannot work — just like my Dad in that class, I happen to know that I am right!

* * *

CLICK ON THE COMIC STRIPS LINK TO SEE MY

“BRIGHT IDEAS” PRESENTATION OF MY BANKING SOLUTION….

(C) 1981 / 2019 Jim Pinkoski